Fintech Innovation Explained for Business Leaders

TL;DR:

- Fintech innovation uses technology to create faster, cheaper, and more accessible financial services for businesses and consumers.

- The most advanced fintech platforms combine AI, blockchain, APIs, cloud, and biometrics to deliver efficient operations and new growth opportunities.

Fintech innovation is defined as the application of technology to create faster, more accessible, and lower-cost financial services by replacing or augmenting traditional banking and payment processes. The global fintech market is projected to reach $324 billion in revenue by the end of 2026, growing at a 25% compound annual growth rate. That number signals a structural shift in how money moves, not a temporary trend. Neobanks like Revolut, AI-powered lending platforms, and blockchain-based payment rails are the most visible examples of what is fintech innovation in practice. For entrepreneurs and business leaders, understanding these forces is no longer optional. The companies that grasp fintech technology explained in operational terms will outpace those still running on legacy financial infrastructure.

What is fintech innovation and what technologies power it?

Fintech innovation is built on five core technologies, each solving a specific limitation of traditional finance. Understanding what each one does helps you evaluate which tools belong in your business.

- Artificial intelligence and machine learning: AI and ML power credit scoring, fraud detection, and personalized financial services. A traditional credit model uses a handful of static variables. An AI model processes thousands of behavioral signals in real time, producing faster and more accurate decisions.

- Blockchain and distributed ledger technology: Blockchain removes the need for a central authority to verify transactions. This reduces settlement times from days to seconds and cuts out intermediary fees in cross-border payments.

- APIs and open banking: APIs and open banking frameworks allow third-party developers to access bank data securely. This is the technical backbone of embedded finance, where financial services appear inside non-financial apps.

- Cloud computing: Cloud infrastructure lets fintech firms scale without building physical data centers. A startup can launch a lending product globally without owning a single server.

- Digital identity and biometrics: Fingerprint authentication, facial recognition, and document verification tools replace paper-based KYC processes. This speeds up onboarding and reduces fraud at the account-opening stage.

Pro Tip: When evaluating any fintech solution, ask the vendor which of these five layers their product operates on. A tool that touches only one layer is a feature. A tool that integrates across three or more is a platform.

These technologies do not work in isolation. The most capable fintech platforms, such as Stripe for payments or Plaid for data connectivity, combine APIs, cloud infrastructure, and AI into a single product layer. That combination is what separates genuine fintech innovation trends from simple digitization.

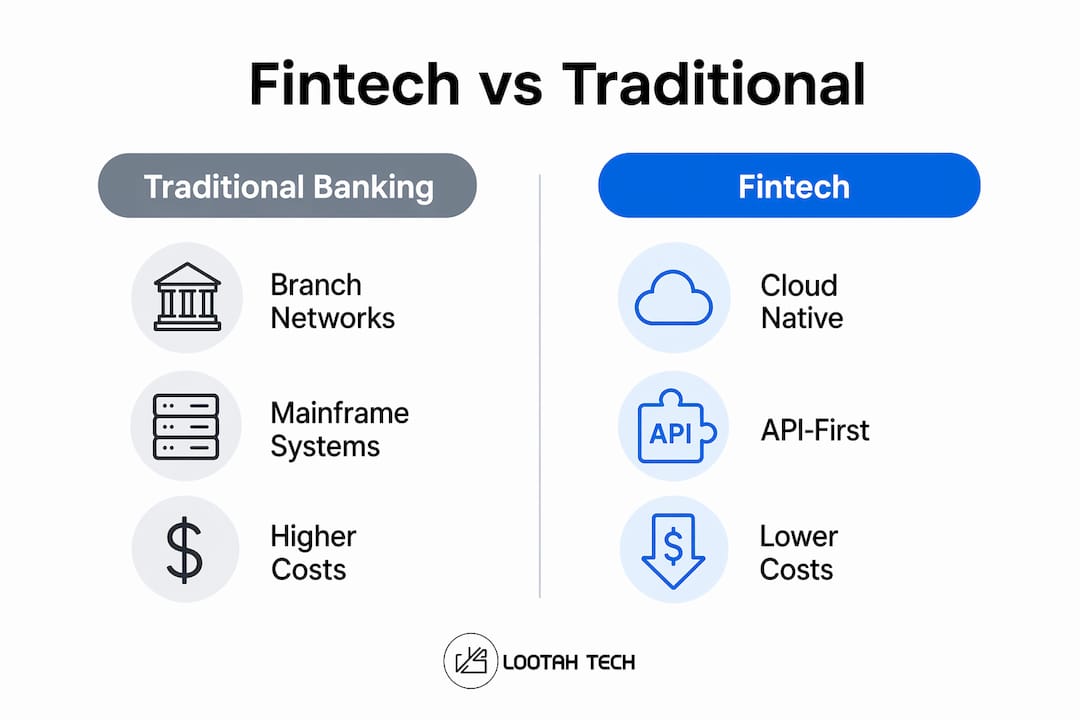

How does fintech differ from traditional financial services?

The difference between fintech and legacy banking is not just speed. It is a structural gap in how each model is built and updated.

| Dimension | Traditional banking | Fintech |

|---|---|---|

| Core infrastructure | Branch networks, mainframe systems | Cloud-native, API-first architecture |

| Product update cycle | Months to years | Days to weeks via continuous deployment |

| Loan disbursal time | Several weeks | 24–48 hours via digital lending platforms |

| Cost structure | High fixed costs from physical branches | Low marginal cost, scales with volume |

| User experience design | Built around internal processes | Built around customer behavior |

| Regulatory posture | Established compliance frameworks | Navigating evolving regulatory environments |

Traditional banks digitized their existing processes. Fintech firms designed new processes from scratch with digital as the default. That distinction matters because digitizing a slow process still produces a slow process.

The loan disbursal comparison is the clearest proof point. Digital lending platforms disburse business loans within 24–48 hours. Traditional bank loans often take several weeks. That gap is not a technology problem on the bank's side. It is an architecture problem. Legacy systems require manual review steps that cannot be automated without rebuilding the underlying workflow.

Pro Tip: Do not evaluate a fintech vendor by its interface alone. Ask how their back-end processes work. A polished app sitting on top of a manual review process is still a slow product.

Fintech firms also carry lower marginal costs because they have no branch networks to maintain. That cost advantage passes to users through lower fees and better rates, which is a core reason the fintech services market is expected to grow from $17.69 trillion in 2025 to $51.08 trillion by 2029.

What are practical fintech applications for your business?

Fintech innovation is not just a consumer story. The operational gains for businesses are substantial and often underestimated relative to the attention paid to consumer-facing apps.

-

Automated accounting and payroll. Platforms like QuickBooks Online and Gusto connect directly to bank accounts and payroll data via APIs. Automated API-integrated tools can reduce manual data errors by 80–90% compared to spreadsheet-based methods. That accuracy gain translates directly into cleaner financial reporting and faster audits.

-

Digital lending and working capital. If your business needs short-term capital, digital lending platforms assess your revenue data, transaction history, and cash flow in real time. Approval and funding can happen within one business day. Traditional bank credit lines require weeks of documentation review.

-

Embedded payments. APIs let you embed payment processing directly into your product or service workflow. A logistics company, for example, can trigger automatic supplier payments the moment a delivery is confirmed, without manual invoice processing.

-

Expense management and business credit. Tools built around business credit card tracking give finance teams real-time visibility into spending by category, department, or project. This replaces end-of-month reconciliation with continuous monitoring.

-

Reaching underserved client segments. Fintech platforms use alternative data to assess creditworthiness for customers who lack traditional credit histories. If your business serves emerging markets or younger demographics, fintech-powered financial products can open segments that traditional banking cannot reach.

Payment data also informs sales strategy in ways that traditional financial reporting cannot. Transaction-level data reveals which products sell fastest, which customer segments pay on time, and where cash flow bottlenecks occur. That intelligence belongs in your growth planning, not just your accounting department.

Fintech innovation is most powerful when it connects to your existing systems rather than replacing them. An API-first integration approach layers new capabilities onto your current infrastructure, preserving operational continuity while adding speed and accuracy.

What challenges should you plan for when adopting fintech?

Fintech adoption creates real operational risk if you move without a clear plan. The following challenges are the ones most likely to disrupt a business that skips due diligence.

- Regulatory compliance. Financial services are regulated at the national and regional level. A fintech tool that operates legally in one jurisdiction may not comply with data residency or licensing requirements in another. Verify compliance coverage before signing any contract.

- Data security and vendor vetting. Skipping rigorous due diligence on a fintech provider's compliance and security infrastructure can cause operational disruptions. Ask vendors for SOC 2 reports, penetration testing records, and incident response documentation.

- Data synchronization. When fintech tools connect to legacy systems via APIs, data can fall out of sync if the integration is poorly designed. Establish clear data ownership rules and audit trails from day one.

- Speed versus risk management. Fintech's speed advantage can tempt leaders to move faster than their risk controls allow. Balancing growth with financial resilience and regulatory compliance is a strategic requirement, not a back-office concern.

- Vendor lock-in. Some fintech platforms use proprietary data formats that make switching difficult. Prioritize vendors who support open data export and standard API protocols.

The most effective adoption strategy is phased. Start with one operational area, such as payroll or expense management, validate the integration, then expand. This approach reduces risk and builds internal confidence before you commit to broader transformation.

Key Takeaways

Fintech innovation delivers its greatest business value when API-first integration, regulatory compliance, and phased adoption replace rushed, wholesale system changes.

| Point | Details |

|---|---|

| Core definition | Fintech innovation applies technology to create faster, lower-cost financial services for businesses and consumers. |

| Five foundational technologies | AI, blockchain, APIs, cloud computing, and biometrics each solve a distinct limitation of traditional finance. |

| Speed advantage | Digital lending platforms disburse loans in 24–48 hours versus several weeks for traditional banks. |

| Operational accuracy | Automated, API-integrated accounting tools reduce manual data errors by 80–90% compared to spreadsheets. |

| Adoption strategy | Use an API-first, phased approach to layer fintech capabilities onto existing systems without disrupting operations. |

What I have learned from watching businesses adopt fintech

Most business leaders I work with treat fintech as a collection of apps. They adopt a payment tool here, a lending product there, and wonder why the efficiency gains never compound. The businesses that get the most out of fintech treat it as an ecosystem, where each tool shares data with the others through well-designed integrations.

The second misconception I see constantly is that fintech is primarily a consumer story. The operational fintech layer, meaning automated payroll, real-time expense tracking, and API-connected accounting, delivers some of the highest returns available to any business. These tools are unglamorous compared to a neobank launch, but they are where the actual margin improvement lives.

I also think the compliance conversation gets buried too late in the process. Leaders get excited about speed and cost savings, then discover a regulatory gap after the contract is signed. Compliance is not a back-end detail. It is a selection criterion that should appear at the top of your vendor evaluation checklist.

The businesses I have seen succeed with fintech share one habit: they define the specific operational problem first, then find the fintech solution that addresses it. The ones that struggle start with the technology and work backward. Fintech is not a strategy. It is a set of tools that executes a strategy you already have.

— YS

How Yslootahtech can power your fintech strategy

Yslootahtech builds AI and machine learning solutions that give businesses the fintech capabilities described in this article, without the complexity of managing multiple disconnected vendors. From automated credit modeling and fraud detection to API-connected financial workflows, Yslootahtech's AI and machine learning services are designed for business leaders who need production-ready systems, not prototypes. The team brings deep experience in fintech architecture across B2B and B2C environments, with a track record that spans digital health, e-commerce, and enterprise finance. If you are ready to move from understanding fintech to deploying it, Yslootahtech is the partner to call.

FAQ

What is fintech innovation in simple terms?

Fintech innovation is the use of technology to deliver financial services faster, at lower cost, and with greater accessibility than traditional banking allows. Examples include digital lending platforms, AI-powered fraud detection, and blockchain-based payments.

How does fintech work for small and mid-size businesses?

Fintech works by connecting to your existing financial data via APIs and automating processes like payroll, lending, and expense tracking. The result is faster decisions, fewer manual errors, and real-time financial visibility.

What are the biggest risks of adopting fintech solutions?

The biggest risks are regulatory non-compliance, poor data security from unvetted vendors, and data synchronization failures between fintech tools and legacy systems. Phased adoption and rigorous vendor due diligence reduce all three.

How is fintech different from traditional banking?

Fintech firms build financial products on cloud-native, API-first architecture designed around user behavior. Traditional banks digitized existing branch-based processes, which preserves legacy inefficiencies even in digital form.

What fintech trends matter most for business leaders in 2026?

The trends with the highest operational impact in 2026 are embedded finance via APIs, AI-powered credit and fraud tools, and real-time payment infrastructure. Explore the top technology trends shaping these developments for a forward-looking breakdown.